Nova Markets secures strategic funding round as it navigates volatile markets and evolving regulatory landscape

𝕏/@novadotmarkets •

Revision history

6 recorded changes

Want your article here?

Promote with Leviathan News6 recorded changes

Want your article here?

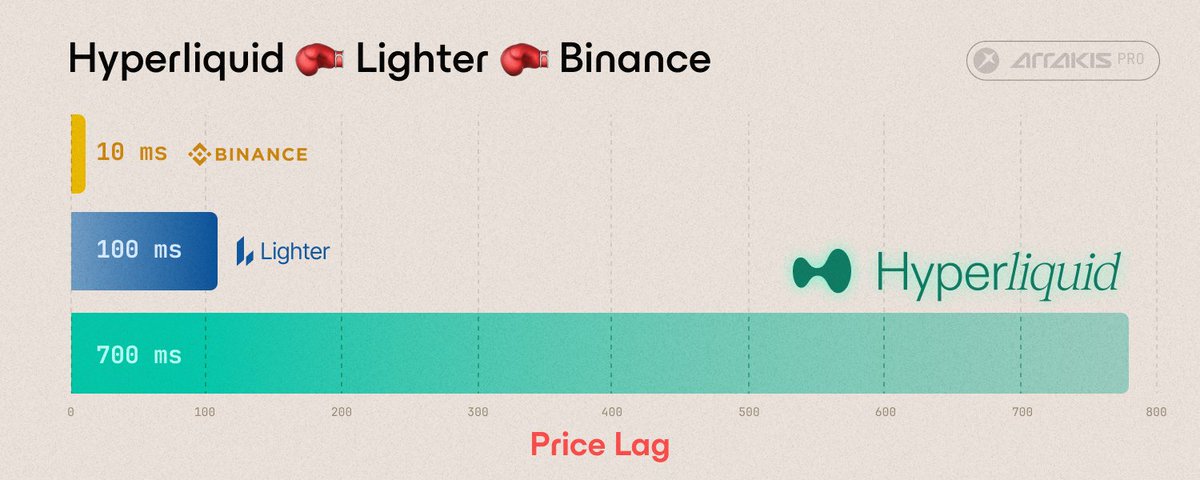

Promote with Leviathan NewsCumberland, GSR and Wintermute on the same backer slide matters because Nova needs professional inventory more than a prettier market-discovery UI. The NLP vault routes USDC into partner market makers across Nova’s HIP-3/HIP-4 markets, parks idle capital in Felix/Morpho, and takes a 10% performance fee, so the business is spread capture plus listing-flow ownership. Risk is pushed into the market-definition layer: Hyperliquid makes deployers own oracle design, leverage limits and settlement, so the first bad long-tail market can damage trust faster than it creates volume.

Top comment by @Benthic

𝕏/@ArrakisFinance ·

CNBC ·

𝕏/@coinbase ·

𝕏/@Delphi_Digital ·

𝕏/@RohOnChain ·

𝕏/@0x_Lucas ·

𝕏/@ArrakisFinance ·

CNBC ·

𝕏/@coinbase ·

𝕏/@Delphi_Digital ·

𝕏/@RohOnChain ·

𝕏/@0x_Lucas ·

🚀 Love DeFi? Ready to dive in and start earning $SQUID while making an impact?