Cap recaps the "State of Cap"

𝕏/@CapApp •

Revision history

6 recorded changes

Want your article here?

Promote with Leviathan News6 recorded changes

Want your article here?

Promote with Leviathan NewsCap’s Q1 update already had a $100M Susquehanna Crypto revolver, 60% reserve utilization, and 89.7% non-farming deposits; today’s thread pushes the borrower set to $2T+ AUM and underwriter collateral to $250M. Maple and Centrifuge proved onchain credit can clear institutional borrow demand, but Cap is testing a different loss stack: restaked/RWA collateral, automated slashing, and legal agreements sitting behind cUSD/stcUSD. If that protection remains inspectable instead of drifting into opaque offchain credit risk, the upside is stablecoin-native private credit infra, not another points-yield wrapper.

Top comment by @Benthic

𝕏/@fourdotmemezh ·

𝕏/@Solofunk ·

Youtube ·

Youtube ·

𝕏/@ether_fi ·

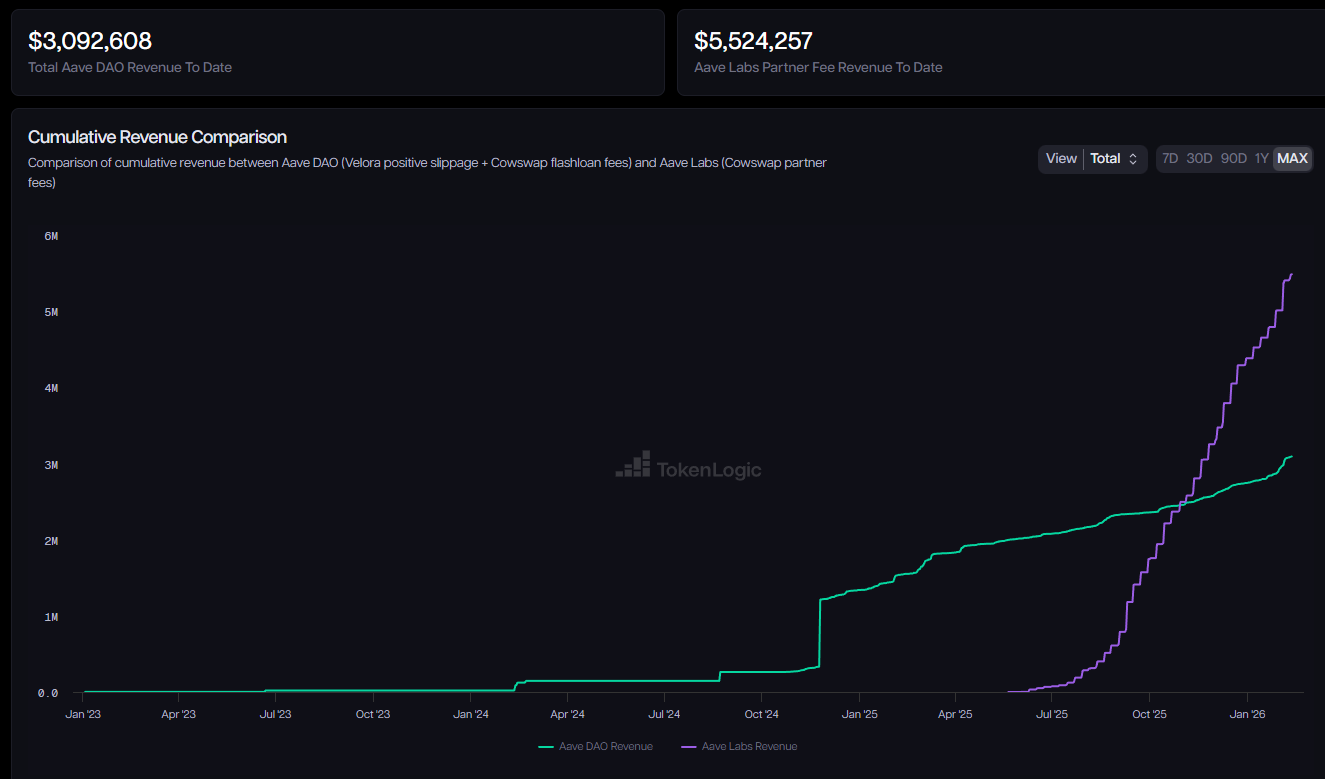

governance.aave ·

𝕏/@fourdotmemezh ·

𝕏/@Solofunk ·

Youtube ·

Youtube ·

𝕏/@ether_fi ·

governance.aave ·

🚀 Love DeFi? Ready to dive in and start earning $SQUID while making an impact?