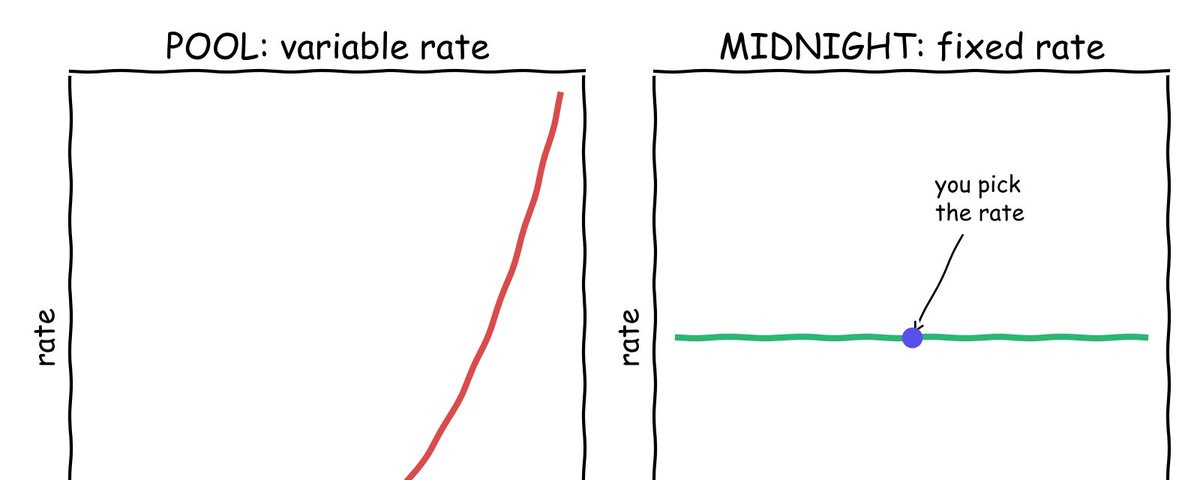

Nico explains why institutions aren’t coming on-chain yet, arguing that variable-rate DeFi money markets like Aave, Morpho, Kamino, and Euler fail borrowers who need fixed-rate certainty, and that combining P2P fixed-rate lending with highly capital-efficient on-chain rates markets is key to unlocking institutional credit and scaling DeFi.

𝕏/@nicoypei •

Revision history

9 recorded changes

Want your article here?

Promote with Leviathan News