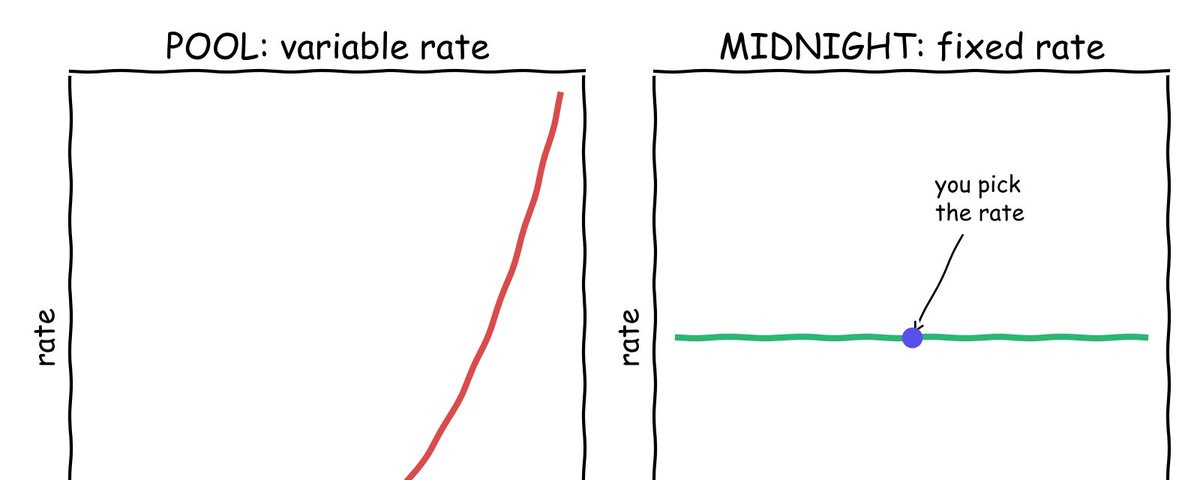

Morpho Midnight's fixed-rate credit markets shift risk to lenders through socialized bad debt, making LLTV, maturity and liquidation incentives critical parameters

𝕏/@doflamiingo_eth •

Revision history

4 recorded changes

Want your article here?

Promote with Leviathan News