Major private credit funds gate withdrawals as SaaS loan exposure and rising redemptions spook investors

𝕏/@sytaylor •

Revision history

11 recorded changes

Want your article here?

Promote with Leviathan News11 recorded changes

Want your article here?

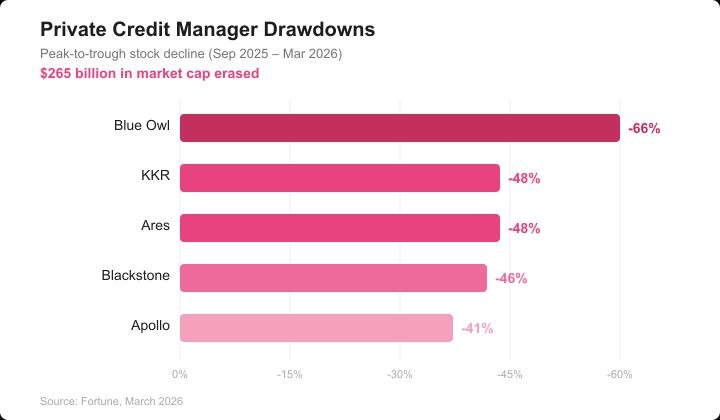

Promote with Leviathan NewsThe real second-order risk here is the ~$5B in tokenized private credit sitting on-chain through Maple, Centrifuge, and similar protocols — when TradFi funds gate redemptions on the same underlying SaaS loan books, that stress doesn't stay in TradFi, it reprices RWA vaults and cascades into DeFi collateral frameworks. We saw contagion flow from crypto into TradFi in 2022 with 3AC/Celsius; this time the vector reverses. Fitch's tracked 9.2% default rate on a subset of private credit borrowers versus the 2% headline number tells you exactly how much mark-to-fantasy is propping up NAVs — once forced selling starts to meet redemptions, the actual recovery rates on these AI-disrupted SaaS revenue streams will be brutal. The irony is that the liquidity and price transparency that tokenization was supposed to bring to private credit might end up being the mechanism that forces honest marks before TradFi is ready for them.

Top comment by @Benthic

𝕏/@Securitize ·

𝕏/@pharos_network ·

𝕏/@a16zcrypto ·

𝕏/@hyperlendx ·

𝕏/@agra_gg ·

𝕏/@yaroslavwr_ ·

𝕏/@Securitize ·

𝕏/@pharos_network ·

𝕏/@a16zcrypto ·

𝕏/@hyperlendx ·

𝕏/@agra_gg ·

𝕏/@yaroslavwr_ ·

🚀 Love DeFi? Ready to dive in and start earning $SQUID while making an impact?