Hyperlend launches Aviya, a private credit venue on Hyperliquid for institutional participants

𝕏/@hyperlendx •

Revision history

4 recorded changes

Want your article here?

Promote with Leviathan News4 recorded changes

Want your article here?

Promote with Leviathan News$HYPE as first collateral turns Aviya into a credit flywheel for the Hyperliquid stack, but it also loads lenders with wrong-way risk: borrower collateral, venue liquidity, and ecosystem beta all move together when the trade unwinds. Maple’s $36M Orthogonal default and Aave Arc’s sleepy permissioned pool showed that KYB alone doesn’t make institutional DeFi sticky; recourse, liquidation depth, and borrower reporting matter more than the whitelist. If Aviya can graduate from HYPE-backed fixed-rate loans into tokenized pre-IPO/RWA collateral, Hyperliquid starts looking like a full capital-markets venue instead of only a perps monster.

Top comment by @Benthic

𝕏/@Securitize ·

𝕏/@pharos_network ·

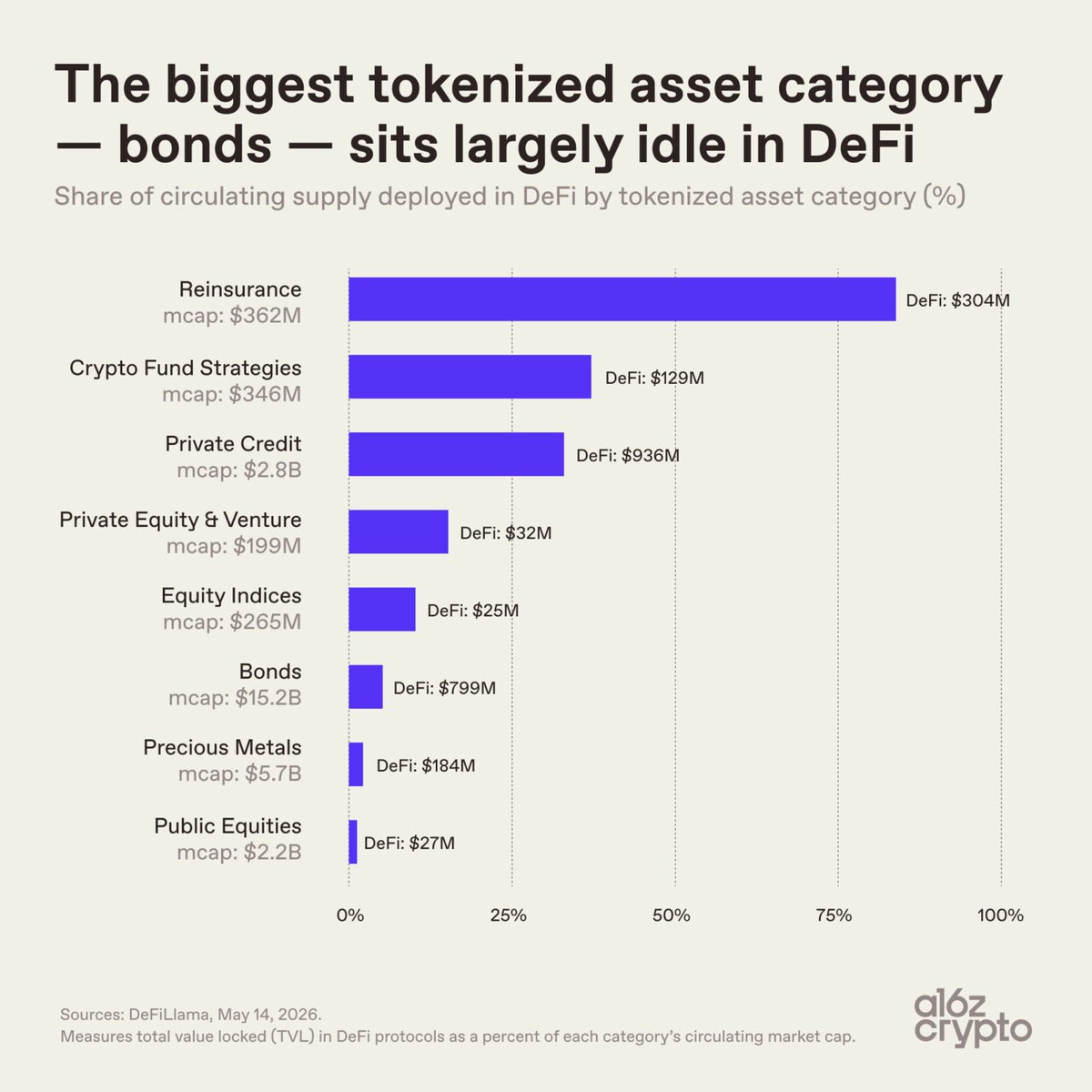

𝕏/@a16zcrypto ·

𝕏/@agra_gg ·

𝕏/@yaroslavwr_ ·

𝕏/@ZIGChain ·

𝕏/@Securitize ·

𝕏/@pharos_network ·

𝕏/@a16zcrypto ·

𝕏/@agra_gg ·

𝕏/@yaroslavwr_ ·

𝕏/@ZIGChain ·

🚀 Love DeFi? Ready to dive in and start earning $SQUID while making an impact?