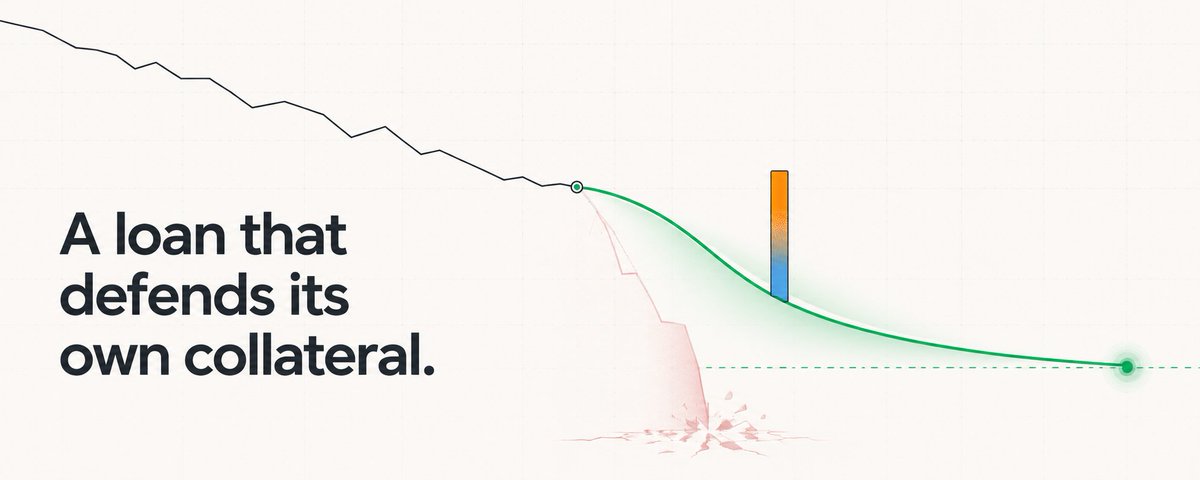

Inspired by Curve's LLAMMA and f(x)'s Liquidation Brake, protocol architect outlines a fixed-rate lending model where collateral self-hedges before liquidation thresholds are breached

𝕏/@0xjayeshyadav •

Revision history

4 recorded changes

Want your article here?

Promote with Leviathan News