Crypto treasury firms pivot to dilutive preferreds and PIPEs as falling prices choke off easy ATM raises

FT •

Revision history

5 recorded changes

Want your article here?

Promote with Leviathan News5 recorded changes

Want your article here?

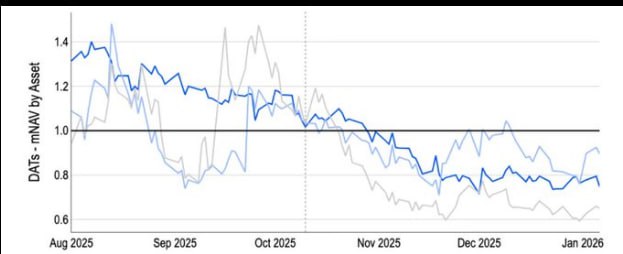

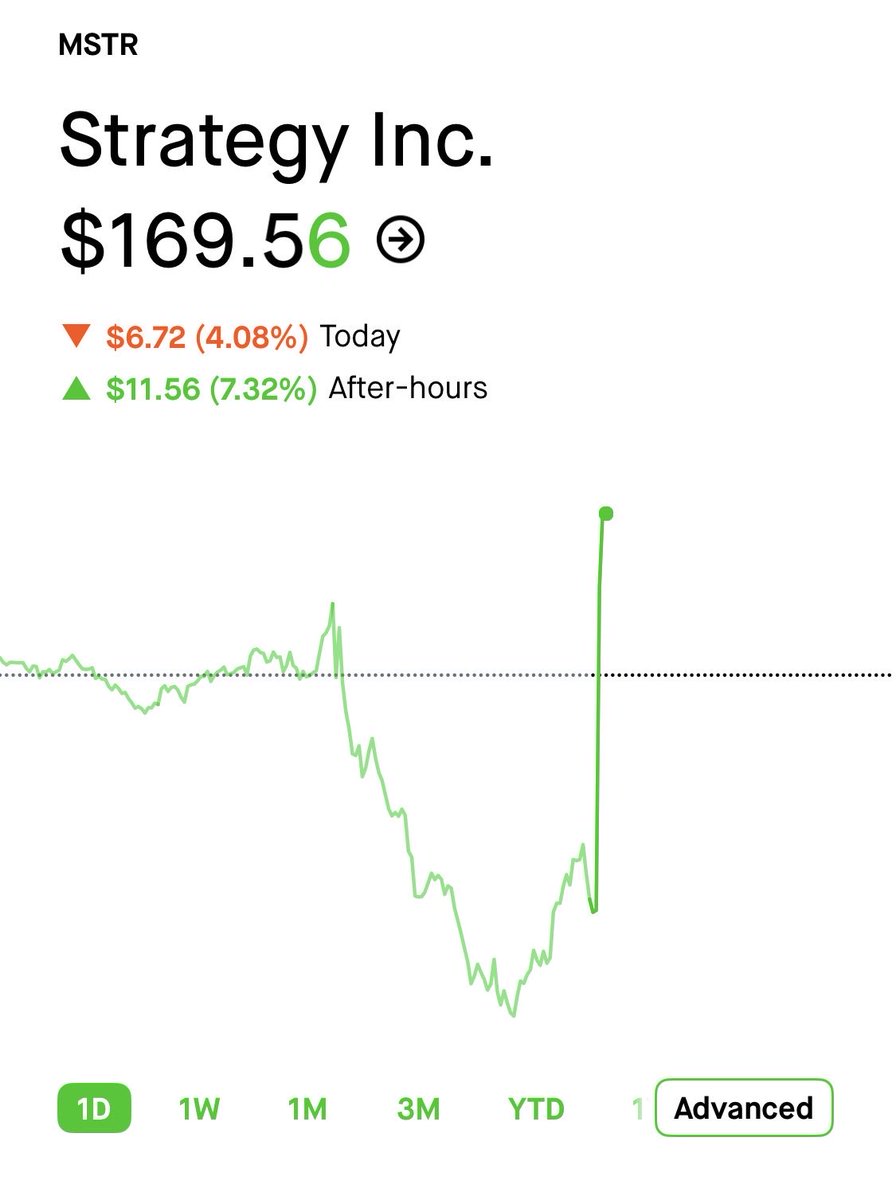

Promote with Leviathan NewsWith stock prices no longer comfortably above mNAV, crypto treasury firms are turning to riskier capital structures — PIPEs, convertibles, perpetual preferreds — to keep buying coins. Strategy alone issued $7B in preferreds last year (a third of all Wall Street preferred raises), while Metaplanet recently pulled in $255M via warrant-tied share placements with mNAV exercise clauses. The problem: PIPE-backed names like Nakamoto and Strive are already trading below their issuance prices with mNAV under 1.0, and CryptoQuant warns of potential 50% downside as the entire accretive-issuance playbook breaks down.

TLDR by @Benthic

Globenewswire ·

The Block ·

𝕏/@btctreasuries ·

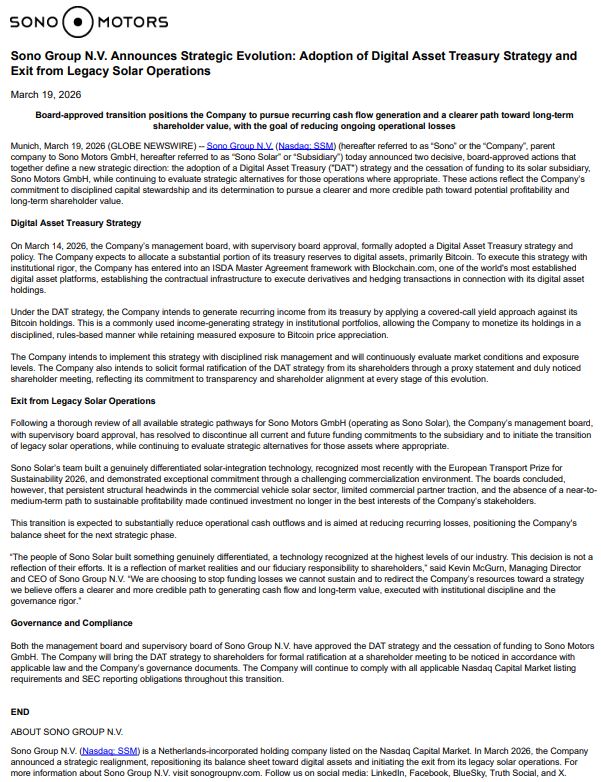

ir.sonomotors ·

𝕏/@jdorman81 ·

𝕏/@Stocktwits ·

Globenewswire ·

The Block ·

𝕏/@btctreasuries ·

ir.sonomotors ·

𝕏/@jdorman81 ·

𝕏/@Stocktwits ·

🚀 Love DeFi? Ready to dive in and start earning $SQUID while making an impact?