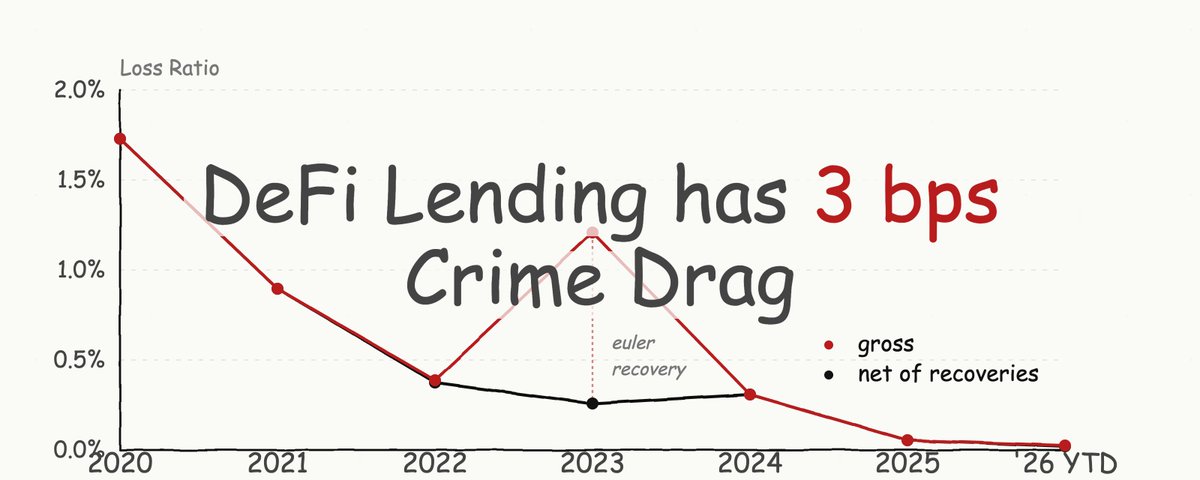

New research argues modern DeFi lending markets are far safer than their reputation suggests, with exploit losses now heavily concentrated in isolated edge cases

𝕏/@flipdazed •

Revision history

8 recorded changes

Want your article here?

Promote with Leviathan News