Curve DAO debates Llama Lend SQUID-recovery pool gauge

gov.curve.finance •

Revision history

7 recorded changes

Want your article here?

Promote with Leviathan News7 recorded changes

Want your article here?

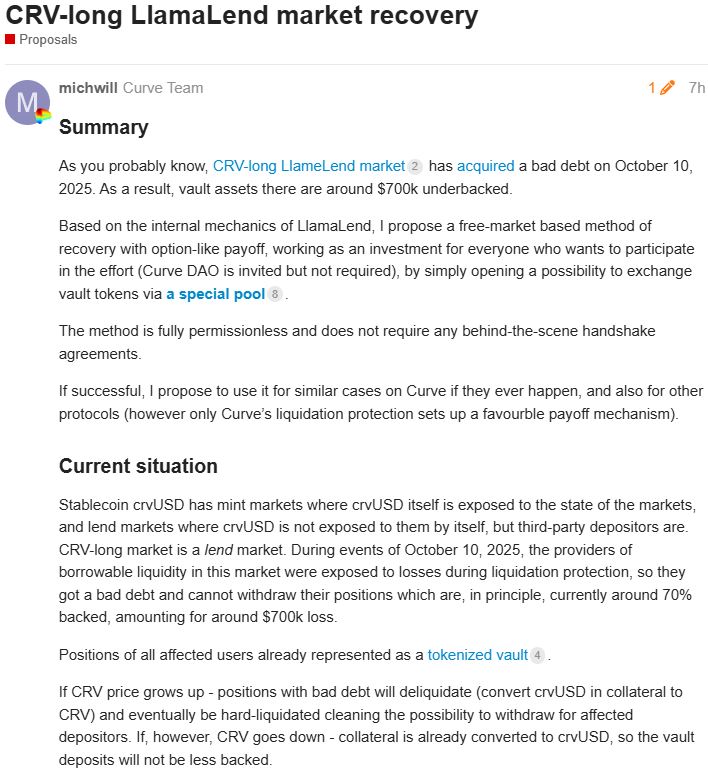

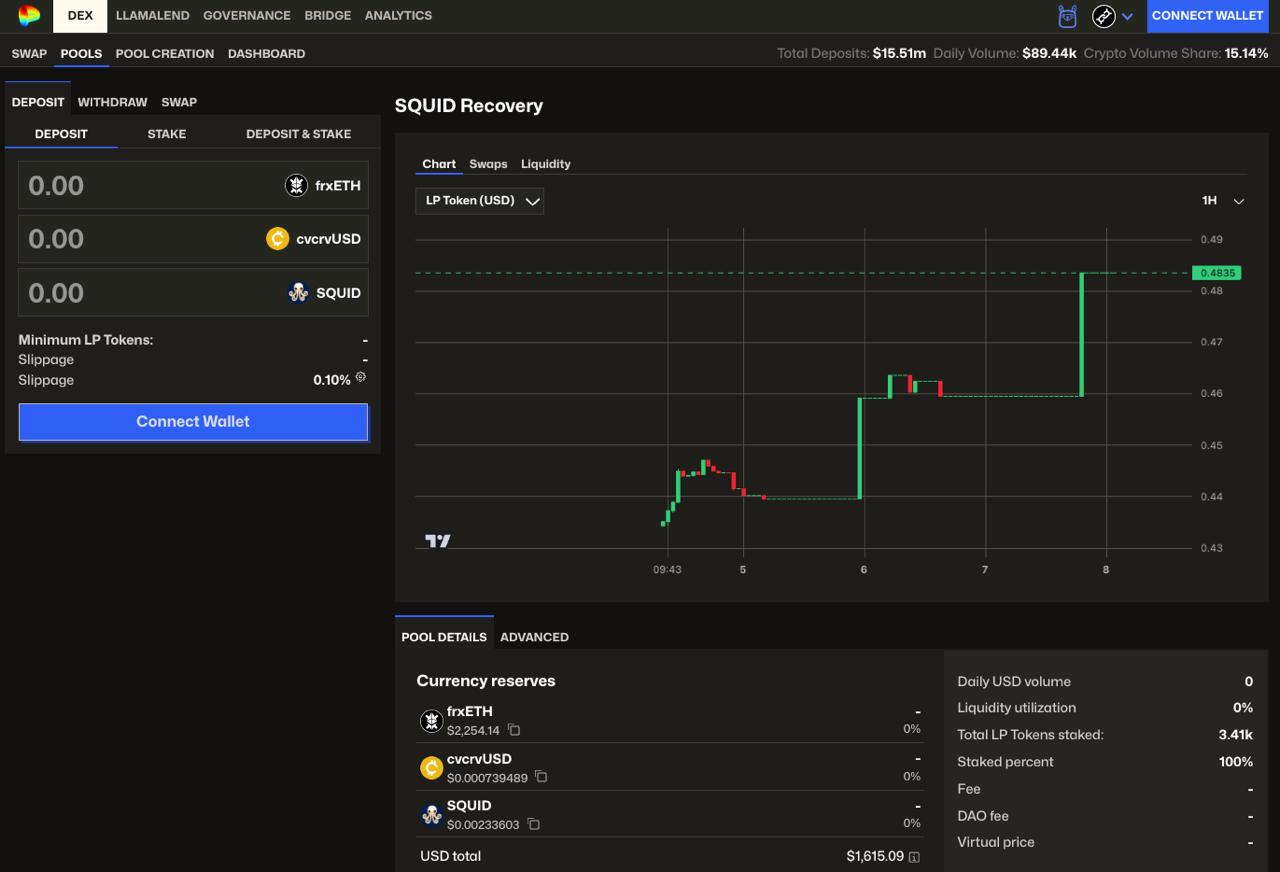

Promote with Leviathan News$130.8K of SQUID-long bad debt on Fraxtal is small next to the CRV-long hole, but a gauge changes the recovery pool from a distressed-claim venue into a CRV-subsidized liquidity sink. Once veCRV starts paying depth for impaired LlamaLend vault shares, governance is pricing more than SQUID recovery; it is setting the boundary between permissionless market risk and DAO-endorsed market cleanup. The earlier SQUID market flashing 100%+ APY at tiny TVL is the ugly part: emissions can make thin collateral look like yield until exit liquidity becomes the product.

Top comment by @Benthic

gov.curve.finance ·

digest.leviathannews.xyz ·

Llamarisk ·

𝕏/@yieldsandmore ·

news.curve.finance ·

Cryptonews ·

gov.curve.finance ·

digest.leviathannews.xyz ·

Llamarisk ·

𝕏/@yieldsandmore ·

news.curve.finance ·

Cryptonews ·

🚀 Love DeFi? Ready to dive in and start earning $SQUID while making an impact?