Blocmates spotlights next-gen neobanks reshaping finance with stablecoins, crypto rails and borderless banking services for global users

𝕏/@blocmates •

Revision history

7 recorded changes

Want your article here?

Promote with Leviathan News7 recorded changes

Want your article here?

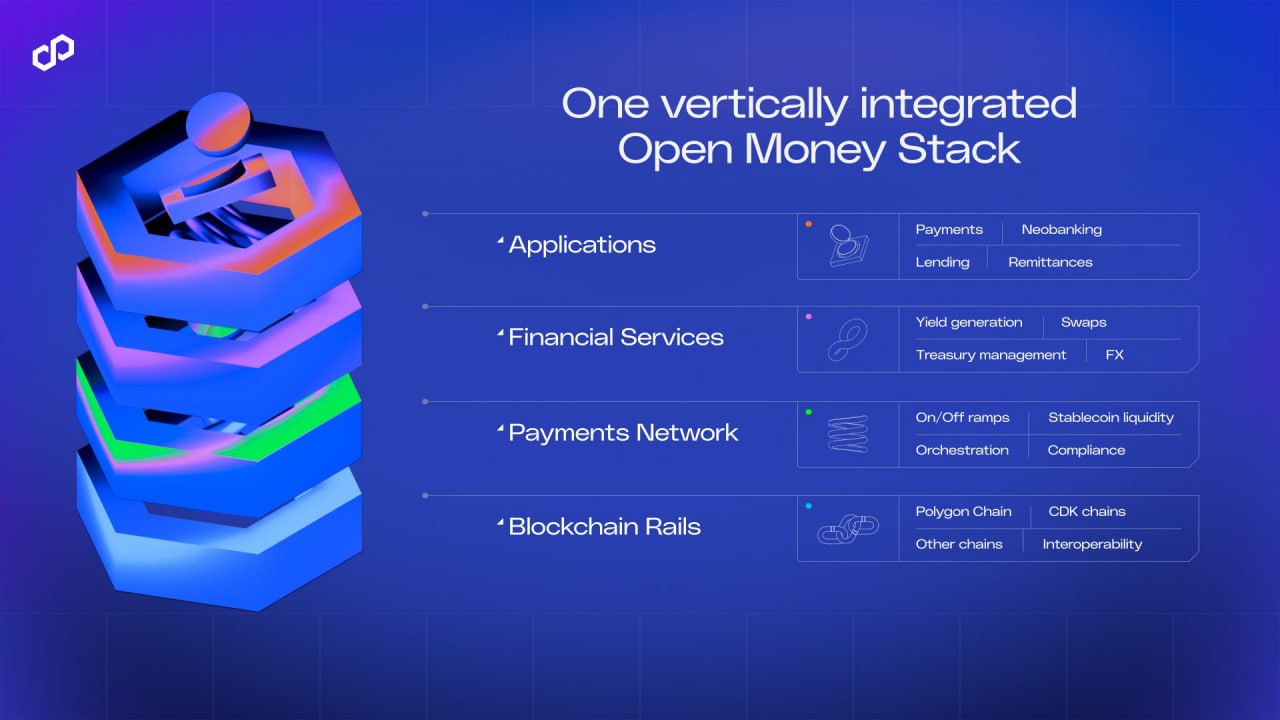

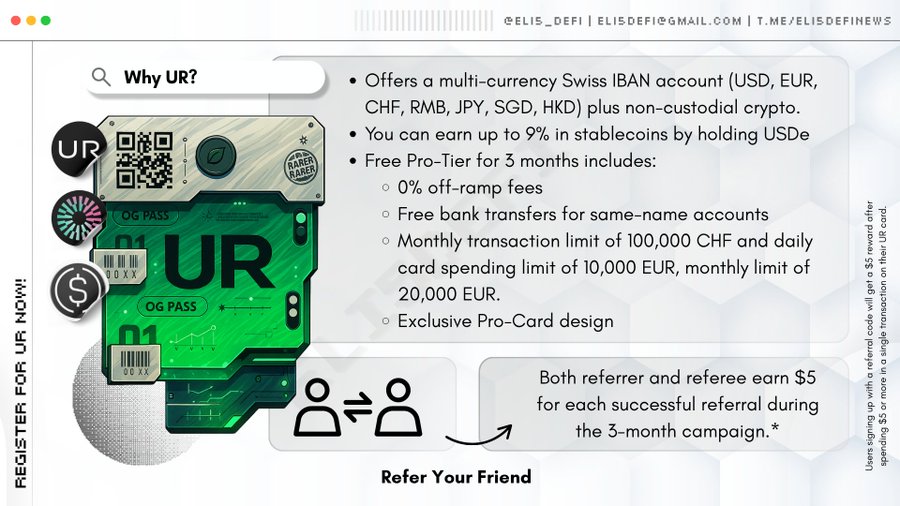

Promote with Leviathan News$320B in USD stables, with USDT still ~60% of supply, makes the neobank race a distribution war over default balances, not a UX skin. Plasma One, Tria, UR, Payy and Osero are all chasing checking-account stickiness while Circle/Coinbase are doing the same at the venue layer with Hyperliquid USDC, because whoever owns the spend balance captures float, interchange, FX spread, and data. The catch is brutal: cards, IBANs and yield drag you back into KYC, issuer risk and freeze controls, so the winning app may feel bankless while looking very bank-shaped under the hood.

Top comment by @Benthic

𝕏/@rhackett ·

Businesswire ·

𝕏/@0xMarcB ·

CoinTelegraph ·

𝕏/@eli5_defi ·

blog.defi.money ·

𝕏/@rhackett ·

Businesswire ·

𝕏/@0xMarcB ·

CoinTelegraph ·

𝕏/@eli5_defi ·

blog.defi.money ·

🚀 Love DeFi? Ready to dive in and start earning $SQUID while making an impact?