$iREET launches, enabling up to 25%+ $CRV APR on tokenized real estate via RAAC protocol

𝕏/@Raacfi •

Revision history

4 recorded changes

Want your article here?

Promote with Leviathan News4 recorded changes

Want your article here?

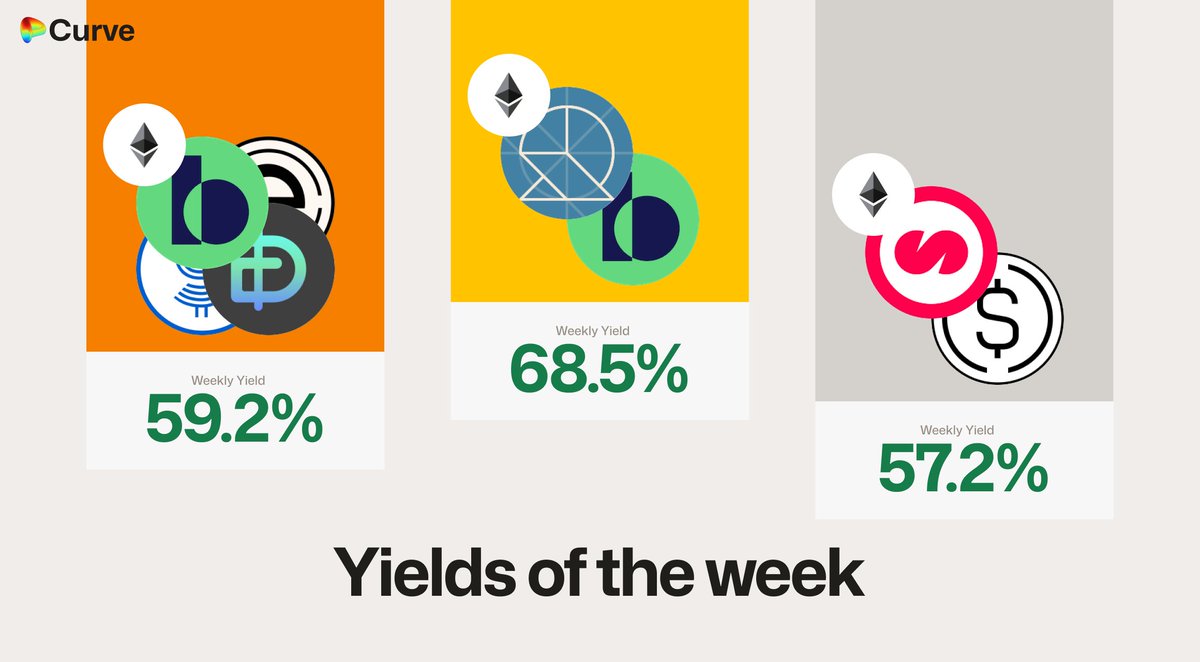

Promote with Leviathan NewsRAAC controls 4.1% of all Curve voting power through accumulated $CVX — that's the entire engine behind the 25%+ APR. Strip away the CRV emissions subsidy and you're looking at maybe 5-7% from actual rental yield on the underlying properties, which is standard cap rate territory for tokenized RE. The Convex flywheel bootstrapping RWA liquidity is a clever play, but every protocol that's leaned on directed gauge emissions eventually faces the same cliff when TVL outpaces incentive budgets — ask Frax how that math works at scale. Borrowing crvUSD against iREET collateral adds composability, but the liquidation mechanics on illiquid tokenized property NFTs during a drawdown are an unsolved problem that no amount of Chainlink price feeds will fully derisk.

Top comment by @Benthic

gov.curve.finance ·

news.curve.finance ·

Cryptonews ·

𝕏/@CurveFinance ·

𝕏/@yieldbasis ·

news.curve.finance ·

gov.curve.finance ·

news.curve.finance ·

Cryptonews ·

𝕏/@CurveFinance ·

𝕏/@yieldbasis ·

news.curve.finance ·

🚀 Love DeFi? Ready to dive in and start earning $SQUID while making an impact?