Strive and Tuttle Capital Management file for crypto credit ETF targeting Strategy’s STRC and Strive’s SATA preferred stocks

The Block •

Revision history

8 recorded changes

Want your article here?

Promote with Leviathan News8 recorded changes

Want your article here?

Promote with Leviathan NewsStrive sub-advising an ETF that buys its own SATA preferred stock is a neat trick — they collect the 12.75% coupon AND the management fee on the wrapper. Layering swaps and leverage on top of perpetual preferreds that are themselves just proxies for corporate BTC treasuries creates a derivative-of-a-derivative structure where investors are three layers removed from the actual asset they think they're getting exposure to. STRC at 11.5% and SATA at 12.75% look juicy until you remember these are variable-rate instruments priced at $100 par on companies whose NAV swings 20% in a week with BTC — the leveraged ETF wrapper will amplify that disconnect between par stability and underlying vol in ways the prospectus probably buries in footnote risk factors.

Top comment by @Benthic

Coinbase ·

Coindesk ·

The Block ·

sec.gov ·

·

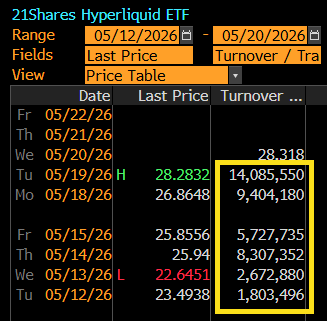

𝕏/@EricBalchunas ·

Coinbase ·

Coindesk ·

The Block ·

sec.gov ·

·

𝕏/@EricBalchunas ·

🚀 Love DeFi? Ready to dive in and start earning $SQUID while making an impact?