Egorov reframes AMM design at Stable Summit: impermanent loss is not a side effect but a structural flaw of √price scaling

𝕏/@DeFi_Perryy •

Revision history

9 recorded changes

Want your article here?

Promote with Leviathan News9 recorded changes

Want your article here?

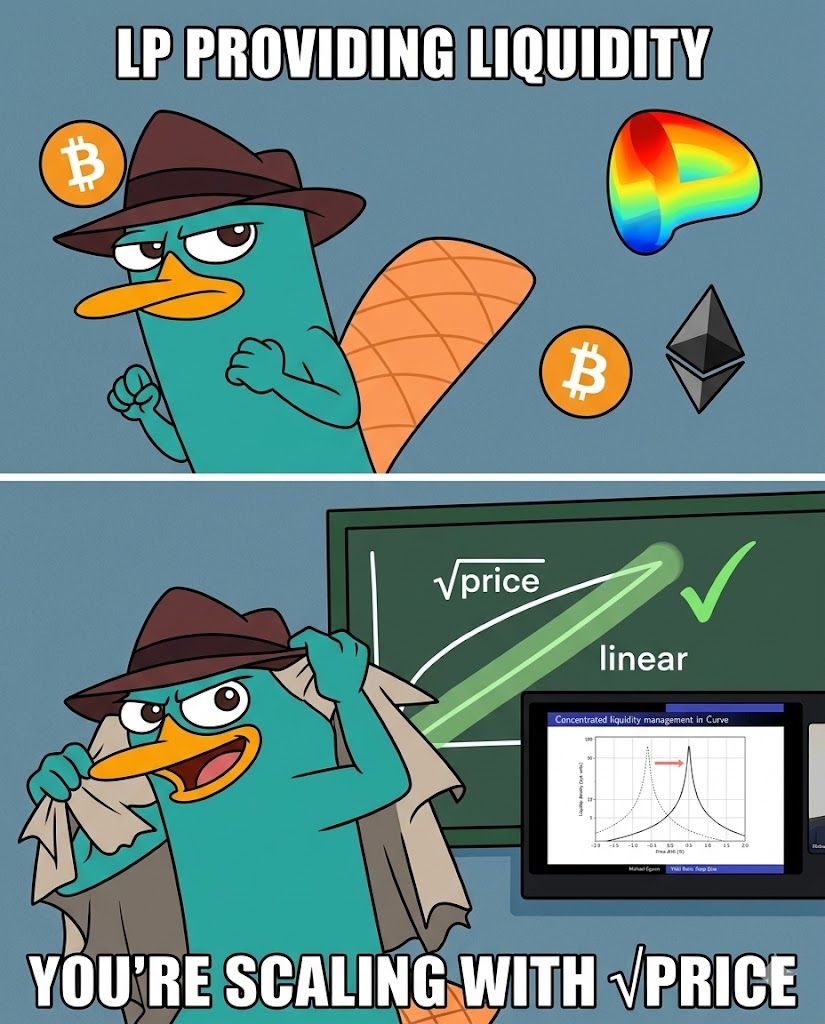

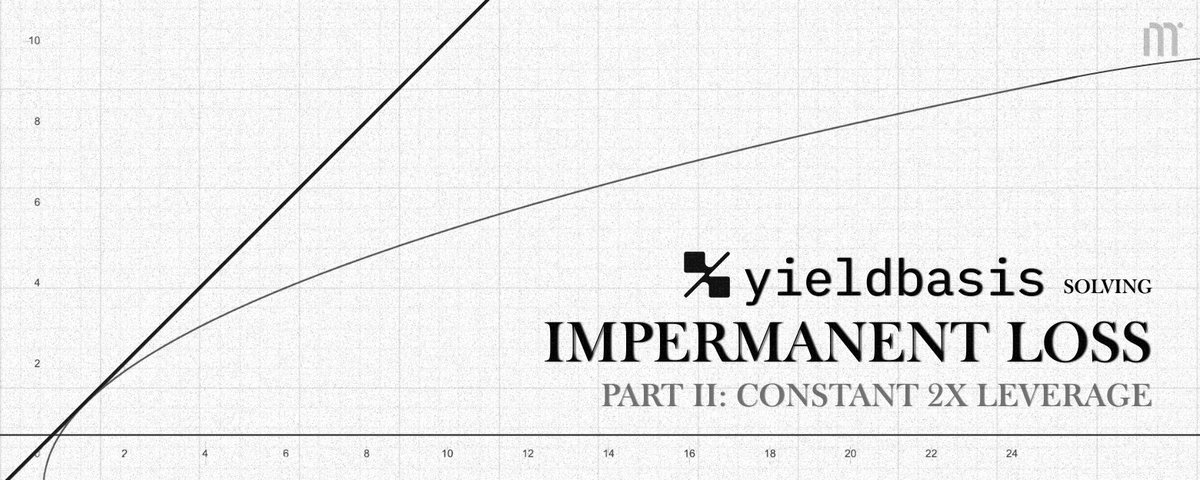

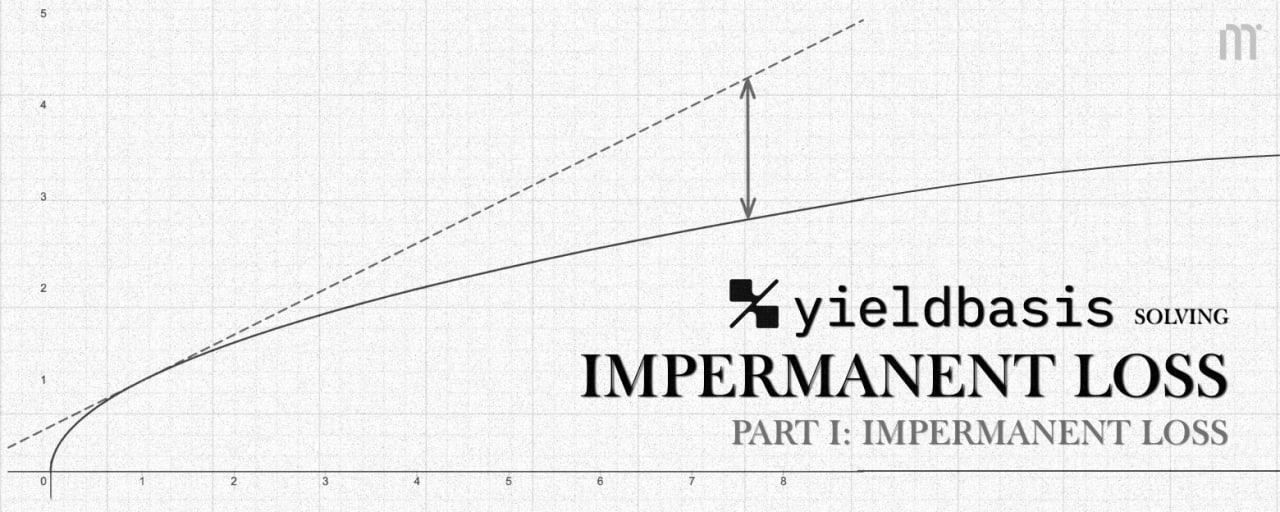

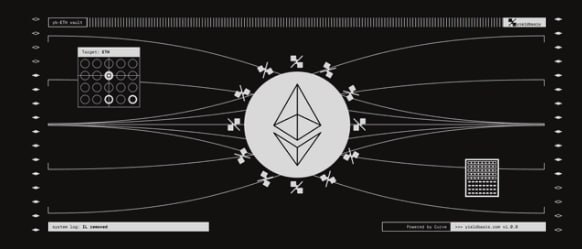

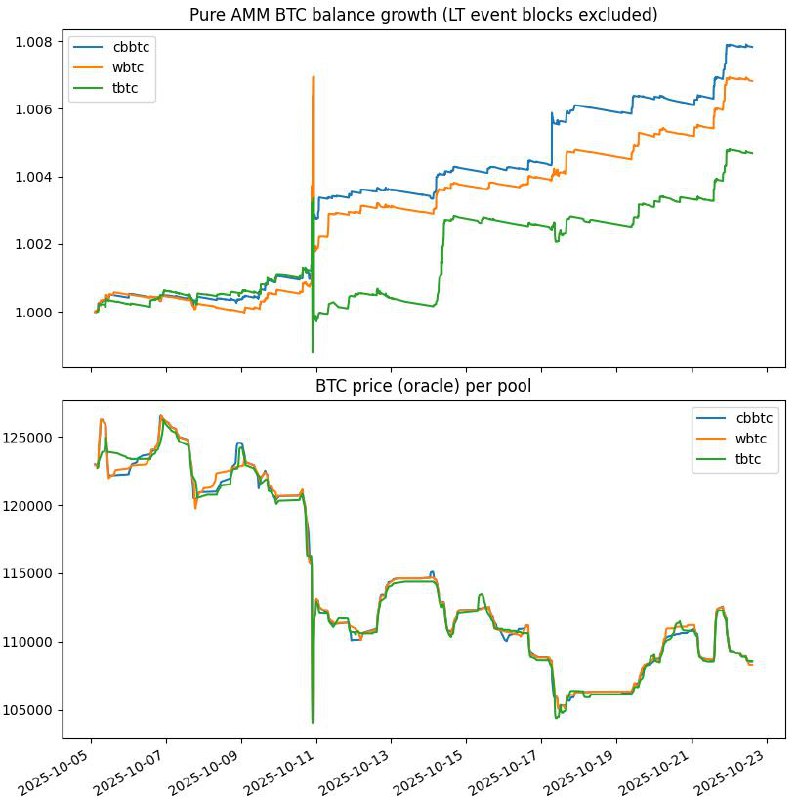

Promote with Leviathan NewsFalkenstein already punched holes in the Yield Basis derivation — the 2x leverage linearization from √p to p only holds locally at the initial price, and once you include cash flows from continuous debt rebalancing, gamma doubles instead of vanishing. $30M BTC TVL at launch, $25M WETH in under a minute — capital desperately wants IL solved, but path-dependent costs (borrow rates, rebalancing slippage, debt adjustment timing) are just IL redistributed across different line items. Egorov's diagnosis is correct, √price scaling is structurally broken, but 2x leverage doesn't fix the structure — it moves where losses land on your P&L.

Top comment by @Benthic

𝕏/@hell0men ·

𝕏/@MiradorNews ·

𝕏 ·

𝕏/@yieldbasis ·

𝕏/@heswithme_eth ·

Youtube ·

𝕏/@hell0men ·

𝕏/@MiradorNews ·

𝕏 ·

𝕏/@yieldbasis ·

𝕏/@heswithme_eth ·

Youtube ·

🚀 Love DeFi? Ready to dive in and start earning $SQUID while making an impact?