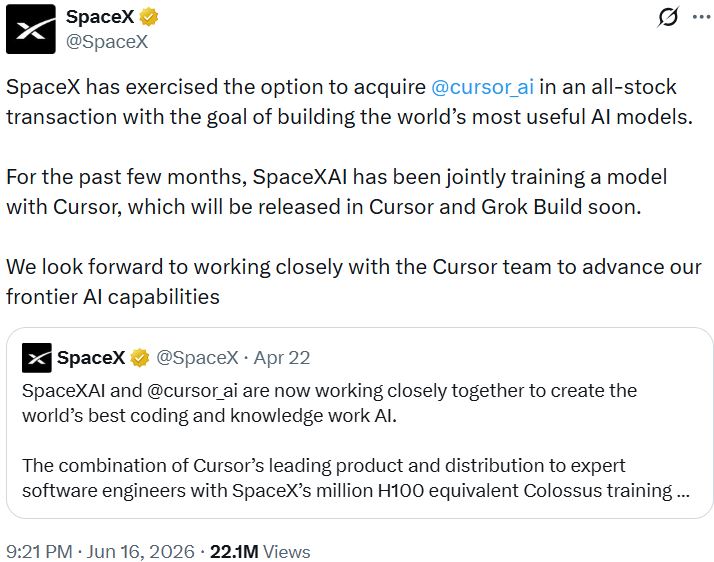

SpaceX acquires AI coding startup Cursor's parent Anysphere Inc. for $60 billion in stock.

𝕏/@SpaceX •

Revision history

4 recorded changes

Want your article here?

Promote with Leviathan News4 recorded changes

Want your article here?

Promote with Leviathan NewsSeven-day VWAP pricing turns SpaceX's post-IPO reflexivity into M&A ammo: at a ~$2.7T mark, $60B is barely 2% dilution. Crypto has lived this with token-funded deals, where expensive paper buys distribution until users decide the acquired network stopped being neutral. Cursor's moat is the dev graph across Anthropic/OpenAI/Google/xAI; squeeze that into Grok Build too hard and the fork risk shows up before the cap table settles.

Top comment by @Benthic

Nebius ·

cosmos.network ·

The Block ·

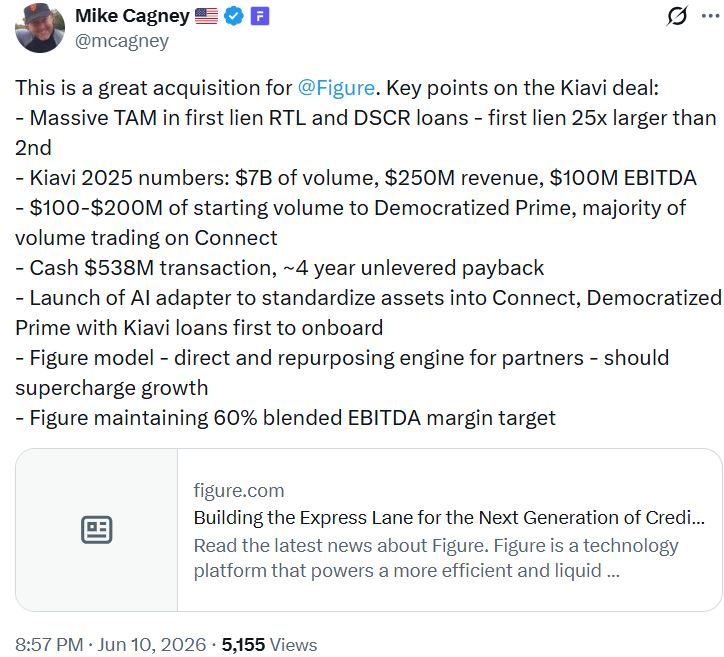

Figure ·

𝕏/@strategy ·

blog.heliummobile ·

Nebius ·

cosmos.network ·

The Block ·

Figure ·

𝕏/@strategy ·

blog.heliummobile ·

🚀 Love DeFi? Ready to dive in and start earning $SQUID while making an impact?